Does Medicare Cover Home Modifications? What's Covered and What's Not

Detailed breakdown of which aging-in-place modifications Medicare, Medicaid, and Medicare Advantage plans will and won't cover.

Some of the hardest conversations our team has with families happen when they realize Original Medicare won’t pay for a walk-in tub or a stair lift. There is a persistent myth that a doctor’s note automatically unlocks funding for home renovations. The reality is that Medicare Part A and Part B have a strict “medical necessity” standard that specifically excludes most permanent home modifications.

But that does not mean you are out of options.

We have spent years analyzing the fine print of insurance policies, and we know that while Original Medicare shuts the front door, other programs often open a side window. The data for 2026 shows a shift: while general Medicare Advantage plans are slightly reducing some home benefits, Special Needs Plans (SNPs) are aggressively expanding them.

This guide explains where the coverage actually exists, the specific forms you need to ask for, and the funding sources most families overlook until it is too late.

The Short Answer Is Complicated

If you ask us for a simple “yes” or “no,” the answer is technically “no” for Original Medicare but “maybe” for everything else. Original Medicare (Parts A and B) is bound by the Social Security Act to cover “durable medical equipment” (DME) but to reject “home modifications.”

The distinction comes down to installation.

Our experts see this denial pattern constantly: if a device attaches permanently to your house (like a ramp or grab bar), Medicare usually classifies it as a “home improvement” and denies the claim. If the device can be easily removed (like a modular ramp or transfer bench), it has a much higher chance of being classified as covered equipment.

What Original Medicare Does NOT Cover

You need to budget realistically for the items that will almost certainly be out-of-pocket expenses. We track installation costs across the U.S., and the numbers for 2026 highlight why relying on Medicare for these big-ticket items is risky.

Original Medicare explicitly excludes:

- Walk-in Tubs: Average installed cost is now $7,800, with luxury models exceeding $15,000.

- Stair Lifts: Straight stair lifts typically cost $3,000-$5,000, while curved custom models can reach $15,000.

- Wheelchair Ramps: Permanent wooden or concrete ramps are considered home improvements.

- Grab Bars: Even with a prescription, the actual bars and installation labor are rarely covered.

- Widened Doorways: Structural changes to accommodate wheelchairs are fully the homeowner’s responsibility.

These exclusions are statutory, meaning Medicare administrators cannot grant exceptions even if they want to.

What Original Medicare DOES Cover

While the renovation exclusion is strict, Part B does cover equipment that serves a similar purpose, provided it meets the definition of Durable Medical Equipment (DME).

Durable Medical Equipment (DME) - Part B

For 2026, the annual Part B deductible is $283. Once you meet that, Medicare pays 80% of the Medicare-approved amount for covered items. You or your supplemental insurance must pay the remaining 20%.

The “Certificate of Medical Necessity” (CMN) is the key document here. Your doctor must certify that the equipment is necessary for use in your home, not just for convenience.

| Equipment | Coverage Status | Estimated Out-of-Pocket (20%) |

|---|---|---|

| Hospital Bed | Covered (with strict criteria) | $200 - $600 |

| Patient Lift (Hoyer) | Covered (manual or electric) | $200 - $600 |

| Commode Chair | Covered (if confined to room) | $15 - $60 |

| Trapeze Bar | Covered (if bed-bound) | $30 - $80 |

| Modular Ramps | Rarely Covered (must be rented/medically necessary) | Varies significantly |

Pro Tip: We often see claims denied because the doctor prescribes a “bathroom renovation” instead of a “3-in-1 commode.” Ask your doctor to prescribe the specific, movable device rather than the structural change.

Medicare Advantage plans often cover home modifications that Original Medicare does not

Medicare Advantage plans often cover home modifications that Original Medicare does not

Home Health Services - Part A

If you qualify for the Home Health Benefit, you have a secondary path to safety improvements. This benefit does not pay for construction, but it pays for the Occupational Therapist (OT) who can design the plan.

Medicare Part A covers:

- Skilled Nursing: Part-time or intermittent care.

- Occupational Therapy: A licensed OT evaluates your home for fall risks.

- Physical Therapy: Rehabilitation to improve safe movement at home.

The OT’s evaluation is arguably the most valuable tool you have. Their official report serves as the clinical evidence you need to apply for grants, Medicaid waivers, or VA benefits.

Medicare Advantage: The Game Changer

Medicare Advantage (Part C) is where the rules change. Private insurers like UnitedHealthcare, Humana, and Aetna have the flexibility to cover “non-medical” services, including home modifications.

But you must look at the specific numbers for 2026 to understand where the value lies.

The Rise of Special Needs Plans (SNPs)

Our analysis of 2026 plan data reveals a critical trend: general Medicare Advantage plans are actually reducing some home benefits, while Special Needs Plans (SNPs) are expanding them.

- General Plans: Only about 21% of standard individual plans cover bathroom safety devices in 2026 (down from 24% in 2025).

- Special Needs Plans (SNPs): A massive 47% of SNPs cover bathroom safety devices, and 72% cover “general supports for living” like housing assistance.

Understanding SSBCI

The magic acronym here is SSBCI (Special Supplemental Benefits for the Chronically Ill). If you have a documented chronic condition—like diabetes, cardiovascular disease, or arthritis—you may qualify for a plan that offers a “flexible spending card.”

These cards often come with an annual allowance of $500 to $3,000 that can be used at approved vendors (like Walmart or CVS) for over-the-counter safety items, including grab bars and raised toilet seats.

How to Find These Benefits

- Check for “Dual Eligible” Status: If you qualify for both Medicare and Medicaid, you likely qualify for a D-SNP (Dual Special Needs Plan), which has the highest home modification coverage.

- Ask Specifically About “SSBCI”: When speaking with an agent, ask: “Does this plan offer SSBCI benefits for my chronic condition?”

- Verify the Vendor Network: Some plans only allow you to buy safety equipment from a specific catalog. Check the catalog before you enroll to ensure it has what you need.

Medicaid Coverage for Home Modifications

If Medicare is the strict parent, Medicaid is the flexible relative—but only if you can get through the door. Medicaid’s Home and Community-Based Services (HCBS) waivers are the primary funding source for major renovations like ramps and roll-in showers.

HCBS Waiver Realities

These waivers allow states to pay for home modifications to prevent nursing home placement. The coverage is substantial, often ranging from $5,000 to $15,000 per project.

However, the demand is overwhelming.

- The Wait: The average waiting time for an HCBS waiver is now 32 months (over 2.5 years).

- The List: According to KFF data, there are over 600,000 people on waiting lists or “interest lists” across the U.S.

- State Variation: States like Texas and Florida have massive waiting lists, while Missouri and North Dakota have virtually none.

Applying Strategic Pressure

Do not just join the list and wait.

- Distinguish “Interest” from “Wait”: Some states have an “interest list” (pre-screening) and a separate “waiting list” (approved but unfunded). You must confirm you are on the official waiting list.

- Emergency Status: If your loved one is currently in a hospital or nursing home and wants to return home, tell the case manager. “Money Follows the Person” (MFP) programs can sometimes bypass the standard waiting list to facilitate a discharge.

A physician-ordered home evaluation is the first step toward Medicare coverage for modifications

A physician-ordered home evaluation is the first step toward Medicare coverage for modifications

PACE Programs

The Program of All-Inclusive Care for the Elderly (PACE) is arguably the most comprehensive option for those who qualify. As of 2026, PACE operates in 33 states (plus D.C.) with nearly 200 centers nationwide.

PACE providers receive a flat monthly fee from Medicare/Medicaid to handle all your care. This incentivizes them to pay for home modifications because installing a $5,000 ramp is cheaper for them than paying for a nursing home stay after a fall.

- Coverage: Extremely broad (ramps, stair lifts, bathrooms).

- Cost: usually free for Medicaid-eligible seniors; Medicare-only participants pay a premium.

- Eligibility: Age 55+, certified as needing nursing home level of care, and living in a PACE service area.

Step-by-Step Strategy to Maximize Coverage

We have successfully guided many clients through this funding maze. Here is the exact checklist we recommend to layer these benefits effectively.

-

Start with the Paperwork. Schedule a home safety assessment immediately. Use the findings to get a “Letter of Medical Necessity” from your primary care doctor. This single document is required for almost every grant and tax deduction.

-

Leverage VA Benefits First. If the homeowner is a veteran, this is your best first stop. The HISA Grant (Home Improvements and Structural Alterations) offers up to $6,800 for service-connected conditions and $2,000 for non-service-connected conditions. You must file VA Form 10-0103.

-

Check Your Medicare Advantage “SSBCI” Eligibility. Call your plan’s support line. Ask specifically: “Do I qualify for Special Supplemental Benefits for the Chronically Ill based on my medical history?” and “Does my plan have a flex card for bathroom safety devices?”

-

File for the Medical Expense Tax Deduction. If you pay out-of-pocket, the IRS allows you to deduct these costs if they exceed 7.5% of your Adjusted Gross Income. This is outlined in IRS Publication 502. The modifications must be for medical purposes, not aesthetic ones.

-

Get on the Medicaid Waiver List Now. Even if you don’t think you need it yet, the 32-month average wait time means you should apply the moment you suspect future need. You can always decline the slot later if you don’t use it.

-

Layer Your Funding. We see families use a Medicare Advantage flex card for grab bars, a VA HISA grant for a ramp, and personal funds for a walk-in tub. There is no rule against combining these separate funding streams to cover a complete renovation project.

The system is designed to be difficult, but it is not impossible. The key is to stop looking for a single “home modification” check from Medicare and start assembling the smaller pieces of coverage—DME, SNPs, and waivers—that build the full solution.

Ready to Take Action?

Learn more about our comprehensive home safety assessments solutions and how they can help your family.

Explore Home Safety Assessments About Margaret Chen

Certified Aging-in-Place Specialist & Senior Care Advisor

CAPS-certified senior care advisor with 15+ years helping families plan for safe aging at home.

Related Articles

How to Budget for Aging in Place: A Family Financial Planning Guide

Step-by-step financial planning guide for aging in place.

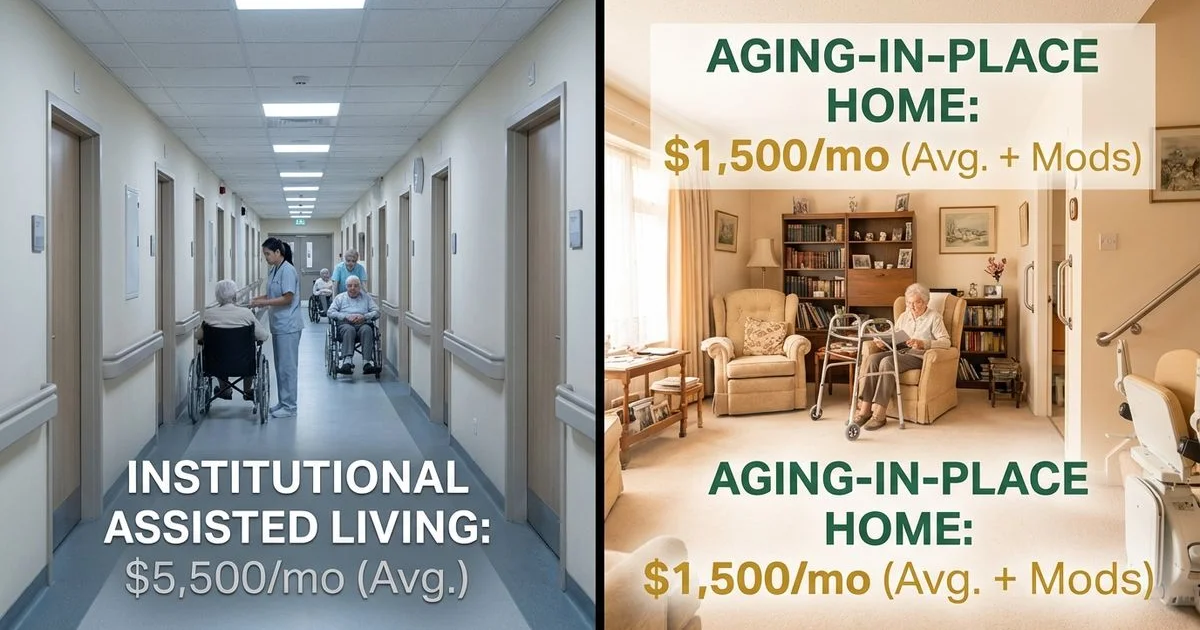

Assisted Living vs. Home Care: True Cost Comparison for 2026

Detailed cost comparison of assisted living facilities versus home care and aging-in-place modifications.

Senior Home Modification Grants, Loans & Assistance Programs

Complete guide to financial assistance for aging-in-place home modifications. Federal grants, state programs, VA benefits, and low-interest loans explained.